Ever feel like your money disappears before the month ends?

It seems like no matter how hard I try, there are weeks when my bank app makes me wince.

Budgeting isn’t always easy, but using a straightforward method takes so much of the stress off my plate. There’s one approach I’m a big fan of: the 50/30/20 rule. It’s a practical way to manage money every month, and it doesn’t feel overwhelming or complicated.

The 50/30/20 rule budget has helped a lot of people, including me, take control of their spending, grow their savings, and keep life a little more balanced.

By the end of this guide, you’ll know exactly how to use the 50/30/20 budgeting method.

You’ll also get budgeting tips, see real-world monthly budget template examples, and find simple ways to stay on track no matter your income or situation.

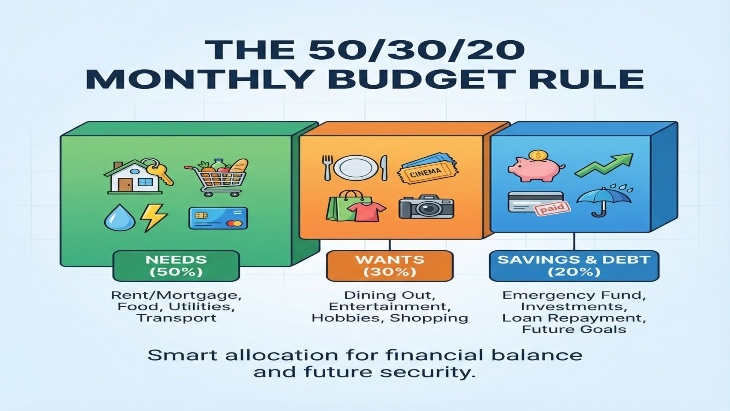

What Is the 50/30/20 Rule?

The 50/30/20 rule is a popular budgeting method developed by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi, as outlined in their book, “All Your Worth.”

It’s become a go-to guideline for people looking to avoid the nitty-gritty of tracking every penny. Instead, you divide your net income (what you get after taxes) into three big categories:

- 50% for Needs: This covers essentials. Monthly bills and basics that you can’t easily skip. Think rent, utilities, groceries, transportation, insurance, and minimum debt payments.

- 30% for Wants: This slice covers life’s perks and luxuries. Dining out, streaming services, hobbies, travel, and all those extras bring some fun.

- 20% for Savings & Debt Repayment: This part goes to your savings account, retirement, investments, and any payments over your minimum debts, like clearing credit card balances faster or padding your emergency fund.

It’s a framework that shows you how to budget your money by keeping things flexible but still direct. The idea is to help make smart choices, without feeling boxed in. (Source: Encyclopedia Britannica)

Why the 50/30/20 Rule Works

Budgeting can feel overwhelming if you’ve never done it, but the 50/30/20 rule is super beginner-friendly.

You split your income into a few clear categories, so you’re not getting lost in endless lines on a spreadsheet. I’ve found it especially helpful because:

- It’s flexible. You don’t have to track every penny; focus on three big chunks.

- It helps you balance the things you need with the things you want, so you’re not totally depriving yourself.

- Savings and debt payments are part of the plan every month, so it’s easier to actually make progress.

- The rule adjusts if your income changes, making it ideal for freelancers or anyone with an unpredictable paycheck.

When I first started, I was afraid I’d have to do math constantly or keep receipts for everything. Instead, this system made it easy to spot where I was overspending (hello, takeout), and simple tweaks had a big impact.

Imagine you make $3,000 a month after taxes.

With the 50/30/20 rule, you’d aim to spend $1,500 on needs, up to $900 on wants, and at least $600 on savings and extra debt payments.

It doesn’t need a bunch of fancy budgeting tools to start, but it works even better with them. More on that below.

Recommended Reading: Jonathan Montoya 5K Sprint In 90days Review: Honest Results

Step by Step: How to Build Your Monthly Budget

Step 1: Calculate Your Net Monthly Income

Your net income is how much actually lands in your bank account after taxes and any payroll deductions (like health insurance or 401(k) contributions). This is your spending power for the month.

If your take-home pay changes from month to month, use a three-month average to figure out a reliable amount to budget with.

This number is your starting point. If you have side hustles or variable income flows (like gig work), include those too, but be conservative with your estimates.

Step 2: List Out Your Monthly Needs

Monthly needs are anything that covers your essentials, the things you couldn’t easily cut out without serious consequences.

Here’s a checklist I use to make sure I’m not missing anything critical:

- Rent or mortgage payment

- Utilities (electricity, water, gas, trash)

- Groceries (not takeout or snacks)

- Basic transportation (gas, public transit, car payment)

- Insurance (health, renter’s, car)

- Minimum loan or credit card payments

- Childcare (if needed)

- Medical expenses (prescriptions, copays)

Hidden needs tip: Double-check for expenses that are often forgotten, like annual bills (spread out as a monthly average), pet care, or essential repairs. These sneak up if you don’t factor them in.

Step 3: List Your Wants

Now it’s time for the fun stuff.

Wants are everything you could dial back if money got tight. These extras make life enjoyable, so it’s good to give yourself permission to spend here, just not at the cost of your future wants or needs.

- Dining out and fast food

- Streaming subscriptions (Netflix, Spotify, etc.)

- Coffee shops

- Shopping for clothes, gadgets, or nonnecessities

- Travel or vacations

- Gym memberships or classes

- Entertainment (movies, concerts, sports tickets)

How to tell a want from a need: Would you still pay for this if you lost your job?

If not, it probably counts as a want. Utilities and groceries are needs, but fancy lattes or a streaming bundle are wants. It sometimes gets tricky, but being honest with myself about these categories made a big difference in my own finances.

Step 4: Allocate to Savings & Debt

This is the category most people ignore, sometimes because there’s nothing left over. With this rule, you build it in from the start.

- Emergency Fund: A separate savings or high yield account that’s there for big surprises (car repairs, job loss).

- Extra Debt Payments: Anything above the minimum, especially for high interest credit cards or loans. This chips away at what you owe much faster.

- Investments or Retirement: IRAs, 401(k)s, brokerage accounts, or even just simple savings for your future goals.

If you’re new to all of this, try automating savings at the start of each month. Even small amounts add up and you won’t feel the temptation to spend if it’s already moved out of your checking account.

Real 50/30/20 Rule Examples

Here are realistic monthly budget template examples using the 50/30/20 rule. These show how it works for different income levels. In case your numbers look different, that’s totally fine—the important thing is understanding the basic split and applying it to your income.

Example 1: Entry Level Job – Net Income $2,500/month

- Needs: $850 rent, $100 groceries, $90 transit, $50 insurance, $60 utilities, $100 loan payment = $1,250

- Wants: Eating out, social activities, new shoes, streaming subscriptions

- Savings/Debt: $150 to savings, $350 extra debt payments

Example 2: Mid Career – Net Income $4,500/month

- Needs: $1,400 mortgage, $300 groceries, $200 transportation, $150 utilities, $200 insurance = $2,250

- Wants: Family dinners out, short getaways, tech gadgets, streaming bundles, fitness classes

- Savings/Debt: $250 to investments, $250 emergency fund, $400 extra toward mortgage or student loan

Tools to Make It Easy

There’s no reason to do budgeting the hard way. Here are some simple tools I recommend:

- Budget Spreadsheets: A basic Excel or Google Sheets monthly budget template is honestly enough to start. You’ll find tons of free options online with built-in 50/30/20 formulas.

- Printable Templates: Good for folks who want to fill things out by hand and stick them on the fridge for motivation.

- Budgeting Apps: There are plenty out there. PocketGuard, Mint, YNAB, and Goodbudget. These sort your spending into categories automatically, track your monthly progress, and even send reminders or alerts if you’re going over.

- Automated Savings: You can set your bank to transfer 20% (or any amount) into savings or to pay off debt automatically on payday. Out of sight, out of mind, and it’s still working for you.

I prefer apps that let me link my accounts and give a quick snapshot of where my money’s going every week. If I notice the “wants” ballooning, I can dial back before it becomes an issue.

How to Adjust If You Can’t Fit 50/30/20

Sometimes my own needs category pushes past 50%, especially in more expensive cities or during emergencies. If your situation is similar, you’re not doing it wrong. The whole purpose of the 50/30/20 rule is to offer a helpful starting point, but life isn’t always so perfectly divided.

- If your needs take up more (say, 60% to 70%), find small ways to trim. Maybe shop for cheaper groceries or negotiate a bill, even if it’s just temporary.

- If saving 20% just isn’t happening this month, put in whatever you can. Even $25 builds the habit and counts for something.

- Once your bigger expenses are under control, try to inch back toward the 50/30/20 split over several months.

Sticking with the principle of balancing needs, wants, and future goals is the real win, not hitting the ratios spot on every month. I’ve had months where my budget was way off, but focusing on progress, not perfection, helped me get things back on track faster.

Common Mistakes to Avoid

- Mixing Wants and Needs: Say you love daily coffee shop visits. It feels essential, but it’s a want. Be straight with yourself and try not to treat luxuries as necessities.

- Ignoring Debt Payments in Savings: Only making minimum card payments and calling it “saving” sets you back, especially with high interest debt. Extra payments matter.

- Not Updating Your Budget Monthly: Life changes all the time. Rent goes up, you cancel a subscription, or you get a new job. Reviewing your categories every month keeps things accurate and less stressful.

- Not Tracking Actual Spending: Sometimes what I plan doesn’t match what happens. Using an app (or even pen and paper) to check in every week or two keeps surprises to a minimum.

Monthly Review Checklist

- Compare how much you actually spent in “needs,” “wants,” and “savings/debt” against your plan. (Most apps do this automatically, but you can also do it in your spreadsheet or notebook.)

- See if you can switch up some spending if you went off track. Move any unspent “wants” cash over to savings instantly.

- Do a quick scan for new subscriptions you forgot or ways you might trim your bills next month.

- Don’t skip celebrating your progress. Savings went up, debt went down, or “wants” didn’t go wild? That’s a win!

Your monthly check-in doesn’t take long, but it’s really important for building money confidence. Use this time to get a feel for your patterns and tweak your budget where needed.

Recap and Next Steps

The 50/30/20 rule makes budgeting way less overwhelming, with simple categories and no need to give a once-over to every detail.

There’s plenty of flexibility to fit any lifestyle. I love that it’s beginner-friendly, but still powerful enough to change how you handle money, pay off debt, and reach your savings goals.

Budgeting isn’t about depriving yourself or saying “no” to everything fun. It’s about taking control, knowing your limits, and being able to treat yourself without guilt.

Whether you use a spreadsheet, a budget app, or a pen and paper, this rule suits nearly anyone and can adjust as life changes. Every small improvement will add up if you stick with it month after month.

If you need a bit of extra motivation, try sharing your goals with a friend or keeping a journaling habit to track wins and lessons learned. The key is to keep things manageable and cheer yourself on as you make progress, even if the numbers don’t match the official ratios every month.

Ready for a Money Makeover? Join the 5K Sprint in 90 Challenge

If you’re looking for a way to turn basic budgeting tips into serious results, it might be time to join the 5K Sprint in 90 Challenge by Jonathan Montoya.

This program is designed to help you build an online business using social media. It’s a beginner-friendly business program that is well-suited if you are someone who has a full-time job or other commitments. Pairing this challenge with your new 50/30/20 system can speed up your progress in a huge way.

➡️ Take the 5K Sprint and start taking control of your life!