Many small businesses look profitable on paper but still find themselves stressing over how to pay rent, cover payroll, or buy supplies next week.

If you’ve ever stared down a stack of unpaid invoices while important bills are due, you know running out of cash can feel overwhelming.

Even when your sales look good in your accounting software, having enough cash on hand is a different story.

Getting a handle on cash flow isn’t about complicated formulas. It’s about building everyday habits and having a system you trust.

By the time you finish this guide, you’ll be set up to understand the big picture and tackle the day-to-day details of cash flow with confidence.

What Is Cash Flow Management for Small Businesses?

Cash flow is all about the money that moves in and out of your business. It sounds simple, but it makes a huge difference in how you operate and grow.

Managing cash flow means staying on top of what’s coming in, what’s going out, and when those things happen. It includes forecasting, monitoring, and making choices to keep your operation running smoothly.

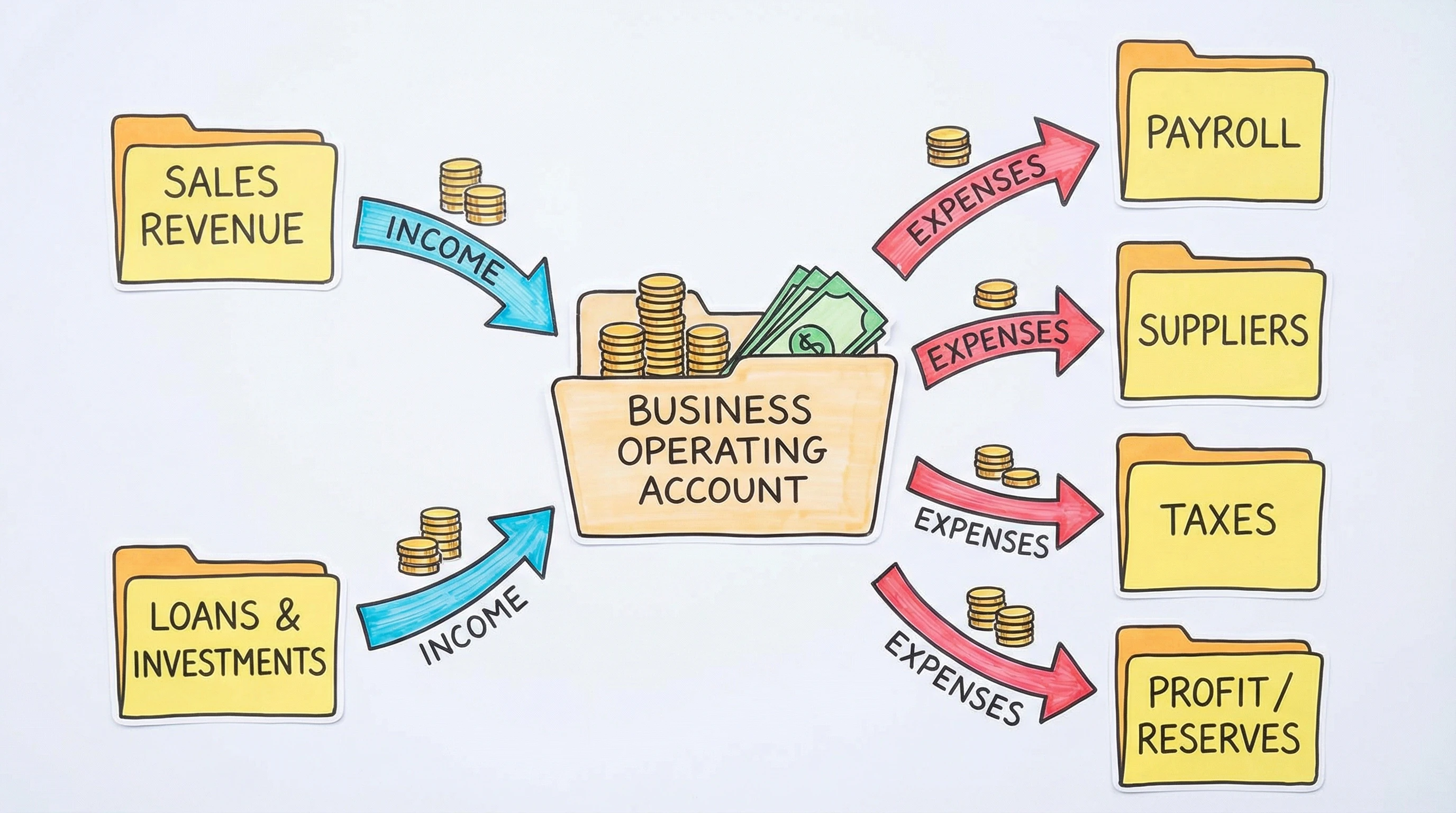

There are three main types of cash flow to keep in mind:

- Operating Cash Flow: Cash from your day-to-day operations like sales, payments to vendors, payroll, and utilities. This is the main area you’ll focus on for most small businesses.

- Investing Cash Flow: Money spent on or earned from buying or selling business assets (like equipment).

- Financing Cash Flow: Money from loans, investments, or repayments you make on debt.

For most small businesses, operating cash flow matters more than the others. Knowing the basics helps you plan. You’ll also be able to spot problems way before they become emergencies.

Jumping into cash flow means not just tracking every transaction, but also making simple projections. Even if you aren’t good with math, regularly estimating your expected income and outgoings can make a real difference. This habit helps you avoid nasty financial surprises and brings peace of mind to your day-to-day work.

Why Cash Flow Management Is More Important Than Profit

Profit looks great on paper, and sure, making a profit is the goal. But profit is an accounting number. Cash flow management deals with real money in your account and the timing of when you receive and spend it.

You can show a $10,000 profit because you’ve made a bunch of sales, but if none of those customers pay for 60 days, you might still be left scrambling when your landlord asks for the rent tomorrow.

Profit helps you know if your business model works. Cash flow keeps your doors open. Even thriving businesses run into trouble if they don’t actively manage when cash arrives and leaves. If you’re mixing personal and business cash, sorting things out gets even tougher. Here’s how separating your finances makes managing cash flow way easier.

Matching expense payments with income receipts can get tricky, especially if your customers pay in irregular intervals. Keeping good records will save you headaches and help you maintain control over your finances.

Always remember: you want to keep enough cushion in your account to pay urgent business bills even when money from customers seems slow.

Common Cash Flow Problems Small Businesses Face

- Late-Paying Clients: Clients often drag their feet on invoices, which quickly locks up your working capital.

- Seasonal Revenue Dips: Many businesses see ups and downs based on the season. Planning for slow months is really important to avoid big cash crunches.

- Overspending on Growth: Buying extra inventory or hiring too soon can dry up your cash well before extra revenues hit.

- Poor Budgeting: Not mapping out your real expenses often leads to nasty surprises.

- Not Setting Aside Taxes: Forgetting about taxes can hit like a wave, fast and hard at the end of the quarter or year.

Cash flow problems can sneak up fast, especially if you haven’t set up basic bookkeeping processes.

One surprisingly popular reason small businesses run into trouble is underestimating slow sales cycles or relying too heavily on a few big customers. Spreading out your customer base and creating reliable billing reminders can help keep your revenue steadier.

8 Practical Cash Flow Management Strategies for Small Businesses

- Forecast Your Cash Flow Monthly: Take 30 minutes at the start of each month to estimate what money you’ll bring in and what you’ll need to pay out. This lets you see potential gaps before they become urgent. Plot your expected income on one side and your planned expenses on the other. Even a hand-drawn chart can help.

- Shorten Your Payment Cycles: Send invoices right after you finish work, not weeks later. Try offering small discounts for early payment and stick to clear payment terms on every contract or invoice. Setting reminders to follow up on unpaid invoices is worth your time.

- Separate Tax Money Immediately: Whenever you’re paid, move a fixed percentage of that income into a dedicated tax savings account. This habit saves tons of stress at tax time.

- Build a Business Emergency Fund: Saving enough for two to three months’ operating expenses gives you a safety net. Even tucking away small amounts each month adds up; this can mean the difference between riding out a slow spell or putting expenses on a high-interest credit card.

- Control Recurring Expenses: Every quarter, review your subscriptions and recurring software costs. Cut anything you’re not actually using. This guide to lifestyle creep applies to business, too.

- Monitor Cash Flow Weekly: Taking five minutes every week to glance at your bank balance, outstanding invoices, and upcoming bills helps you spot trends and avoid last-minute surprises. Weekly touchpoints make it easier to catch potential problems early and adjust your plan as needed.

- Avoid Mixing Personal and Business Spending: Use separate bank accounts and cards for business stuff to keep your records clean and make analysis way easier. Doing this also ensures that you won’t mix up personal spending with deductible business expenses at tax time.

- Reinvest Strategically: Investing in your business is great, but keep an eye on liquidity. Never invest cash you’ll need for next month’s bills. Look for investments you’re truly ready for, not what feels exciting in the moment. .

Establishing these habits can help your business build stability, reduce stress, and lower the risk of surprise cash shortages.

If you make these adjustments part of your regular routine, you’ll steady your finances and save time in the long run.

Simple Cash Flow System for Online Entrepreneurs

Keeping your system straightforward goes a long way, especially if you’re running a modern, mostly online business.

Here’s one way I keep cash organized:

- All business income lands in your Operating Account.

- A fixed percentage of every deposit moves into a Tax Account; don’t touch it until you pay taxes.

- Transfer your personal income to your Owner Pay account. This is your paycheck.

- Regularly move a percentage to a Reserve Fund (your emergency fund).

- Any leftover funds can be put toward Growth or Investment accounts, saved for bigticket expenses or future expansion.

If you use accounting software, you can often automate transfers between these accounts, saving yourself time and mental energy every month.

Mistakes That Kill Small Business Cash Flow

- Counting Sales as Cash: Waiting for payments? That’s not real cash until it’s actually in your bank account.

- Forgetting About Taxes: All it takes is one big tax bill to break your stride if you’re not consistently setting cash aside.

- Expanding Too Fast: Getting overly optimistic about growth and hiring or buying inventory too soon dries up your available cash.

- Overusing Credit: Relying on credit to cover ongoing expenses racks up interest quickly and hides underlying money issues.

- Not Reviewing Your Numbers Regularly: Out of sight, out of mind, and ignoring cash flow details almost always leads to mistakes down the line.

Other common missteps include not following up on late invoices or using business funds for personal expenses. Avoid these to help keep your business finances stable and manageable.

Want to Build a Business With Strong Financial Foundations?

Separating your personal and business finances is a powerful first step. But if you truly want to build something sustainable — something that generates consistent income without constant financial stress — you need the right foundation from day one.

If you’re serious about building a sustainable income, I’ve put together a free training bundle to help you move forward with clarity and confidence.

Inside, you’ll get:

Free access to 4 powerful masterclass videos

A beginner-friendly guide to building online income streams

Practical strategies to grow revenue while maintaining financial clarity

It’s designed to help you not only earn online, but manage and scale your income the smart way.

Access the free training bundle here and start building your business on solid financial ground.

Frequently Asked Questions

Q: Is cash flow the same as profit?

A: Cash flow is the actual money moving in and out of your business. Profit is what’s left over after expenses, and it can include sales you haven’t actually been paid for yet. You need positive cash flow to keep things running, even if your books say you’re profitable.

Q: How much cash reserve should a small business have?

A: It’s smart to aim for two to three months of your normal operating expenses. This buffer helps you cover bills in slow times or emergencies without scrambling to borrow money.

Q: How often should I review my cash flow?

A: Give your cash flow a quick scan weekly and do a more detailed review every month. The weekly checkup keeps you from getting blindsided, while the monthly review helps you plan bigpicture moves.

If you want a straightforward framework for structuring your business accounts, paying yourself, managing taxes, and keeping those uncomfortable financial surprises away, I’ve put together a free financial blueprint.

Grab it here and start getting your small business cash under control today.