Ever read a financial article and feel lost in jargon?

APR, compound interest, net worth—it feels like a foreign language. Financial literacy really matters, yet nobody seems to teach it in school.

The long list of strange money terms can be intimidating and keeps a lot of people from taking charge of their finances. If you’ve ever put off budgeting, investing, or even opening a savings account because the words alone felt overwhelming, you’re definitely not alone.

There’s good news: you don’t need an advanced degree to get a handle on your money. Once you know the basic terms, your confidence really grows.

Whether you want to build savings, pay off debt, or finally start investing, it all starts with understanding a few important words.

This guide breaks down the 30 most important personal finance terms you need to know, explained in plain English. By the end, reading financial content and making money moves on your own won’t seem nearly as confusing.

Essential Budgeting Terms

Setting up a budget is the real foundation of personal finance.

Knowing a handful of simple terms can make budgeting feel way less overwhelming, even if you’re brand new to it.

Here are the big ones worth knowing right away:

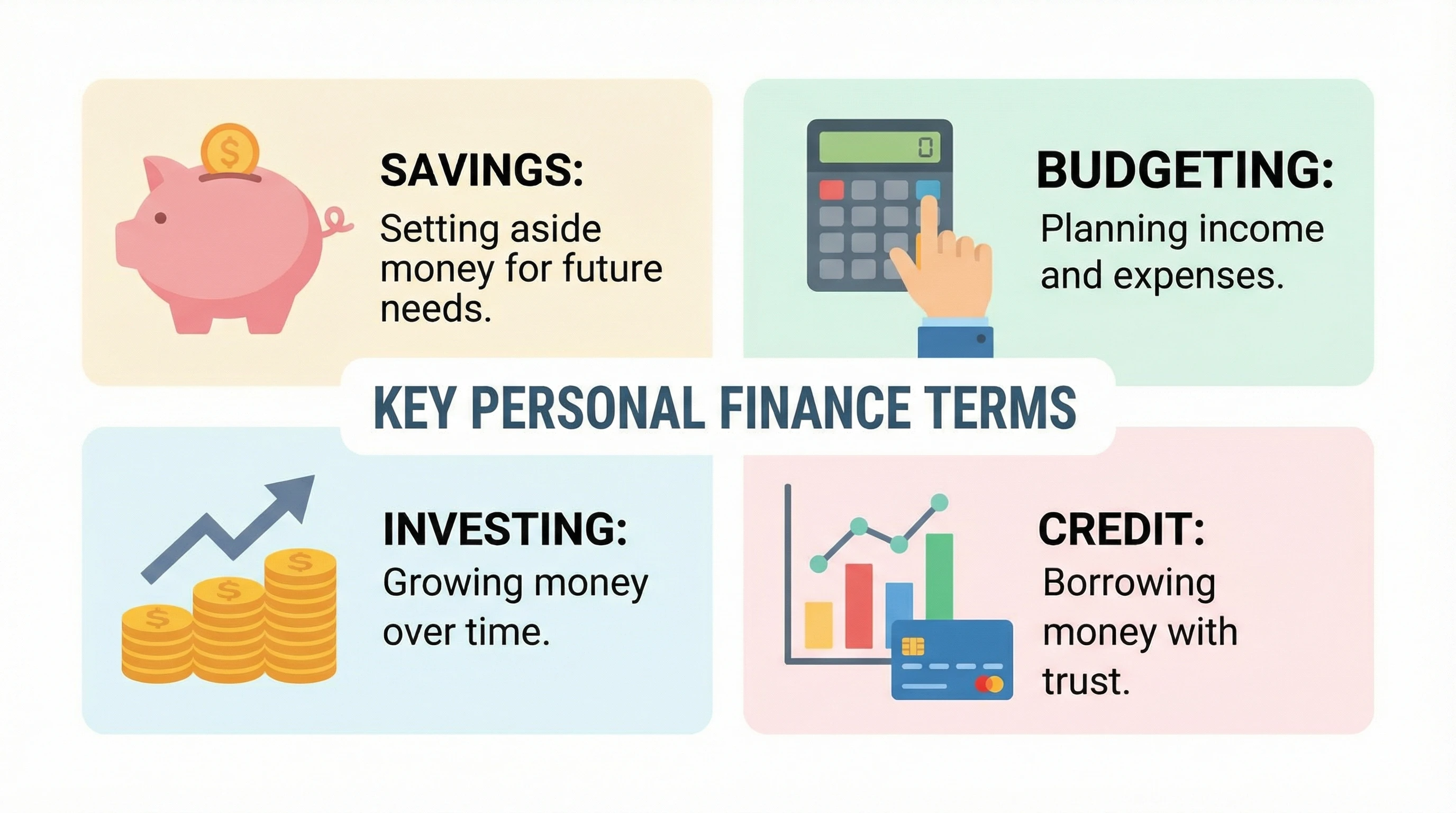

- Budget: A budget is your plan for how to spend money over a specific period, usually each month. It lays out exactly where your cash goes, covering both your spending and your saving. Budgets help curb impulse spending and make sure you’re working toward your goals.

- Income: This is the money you earn from your job, side hustles, investments, or any other sources. There are two types: gross income (your pay before taxes and deductions) and net income (what actually lands in your account after taxes).

- Expenses: These are all the things you spend money on. Fixed expenses (like rent or subscriptions) stay the same each month, while variable expenses (like groceries or entertainment) can change. Keeping an eye on both is super important for sticking to your budget.

- Cash Flow: Cash flow is the balance between money coming in and money going out each month. Positive cash flow means you’re bringing in more than you’re spending, which is pretty handy for growing savings or paying down debt.

- Emergency Fund: This is a stash of savings set aside for those “uh-oh” moments, like losing your job or unexpected bills. Having three to six months’ worth of expenses safely tucked away helps protect you from financial emergencies. Check out my article on how to start an Emergency Fund.

- 50/30/20 Rule: This is a simple framework for managing your budget. Spend 50% of your take-home income on needs, 30% on wants, and put 20% toward savings or debt repayment. It’s a popular starter strategy for getting your finances in order.

Another budgeting tip is to track your spending habits. Use a notebook, a spreadsheet, or an app. This can open your eyes to unconscious spending, helping you see areas where you might cut back and giving you extra money for your goals.

Many people are surprised how much small purchases add up by the end of the month. Plus, tracking every dollar you spend is one of the best ways to stay on budget over the long haul. If you tend to overspend in certain categories, like dining out or shopping online, keeping tabs helps you adjust before things get out of hand.

Recommended Reading: How To Build A Monthly Budget Using The 50/30/20 Rules

Understanding Debt and Credit

Dealing with debt and knowing how credit works are huge parts of personal finance.

These eight terms come up all the time, and knowing what they mean makes it a lot easier to borrow smart, manage credit cards, and build a good financial reputation.

- Credit Score: A number ranging from 300 to 850 that shows lenders how reliably you handle borrowed money. Scores are based on payment history, debt owed, length of credit, and more. A higher number makes it easier (and cheaper) to borrow money, rent apartments, or even land a job in some cases.

- APR (Annual Percentage Rate): APR means the total cost of borrowing, including interest and fees, spread out over one year. If you take out a $1,000 loan at a 10% APR, it’ll cost you $100 a year if you don’t pay it off. Comparing APRs makes it easier to find good deals on loans and credit cards.

- Interest: This is the extra money you pay when borrowing money (like on a credit card or loan), or the money you earn from savings and investments. There are two main types: simple interest (based only on the original amount) and compound interest (interest that builds on itself, which grows much quicker over time).

- Principal: The starting amount you borrow before adding any interest or fees. Let’s say you take out a $5,000 car loan; that $5,000 is your principal. The lower your principal, the less you’ll pay in the long run.

- Credit Utilization: This is the percentage of your total available credit that you’re using. For example, if you have $5,000 in credit limits and owe $1,000, your utilization is 20%. Most experts suggest keeping this under 30%. Lower is better for your credit score.

- Debt-to-Income Ratio (DTI): Your monthly debt payments divided by your monthly gross income, usually shown as a percentage. If you pay $500 in debt each month and earn $2,000, your DTI is 25%. Lenders use this to decide if you’re able to take on more debt responsibly.

- Debt Snowball: A method for paying off debt by attacking your smallest debts first while making minimum payments on larger ones. Each time you pay one off, you roll those payments into the next debt. This helps build motivation with quick wins.

- Debt Avalanche: With this approach, you pay off debts with the highest interest rates first. It saves more money on interest over time, but the psychological wins might not show up as quickly as with the snowball method.

It’s also vital to understand the difference between good debt and bad debt. Good debt, like a reasonable mortgage or a student loan, typically helps you acquire an asset or increase your earning potential.

Bad debt, like high-interest credit card balances for unnecessary purchases, drags you down with high fees and doesn’t add value. Keeping your credit history clean by paying bills on time and not maxing out your cards will help you keep your options open when you want to buy a home or car.

Lenders also check your credit report, which details your credit accounts, payment history, and inquiries made by lenders. Annually, you’re entitled to request a free copy of your credit report from each of the three main credit bureaus—Equifax, Experian, and TransUnion.

Check them periodically to spot errors and correct them right away, since errors could hurt your credit score or impact future loan approvals. If you’ve been denied credit or suspect identity theft, reviewing these reports becomes even more important.

Responsible credit card use also pays off. Try to pay off your balance in full each month to avoid paying high interest.

If that’s not possible, always pay at least the minimum amount on time to avoid damaging your credit score. Periodically ask your card issuer for a higher limit—if you don’t add charges, this lowers your credit utilization and can boost your score.

Investment and Savings Terms Explained

Building wealth isn’t just about saving—it’s about growing your money, too.

Here are ten key terms to help you understand the world of investing and long-term savings, even if you’re starting small.

- Savings Account: This is a basic bank account that pays you a small amount of interest on your cash. It’s safe, FDIC insured, and great for emergency funds or short-term savings.

- High-Yield Savings Account: These accounts are usually offered by online banks and pay much higher interest than regular savings accounts. More interest means your savings grow faster, even without extra effort.

- Investing: Putting your money into things you guess will grow in value, like stocks, bonds, or funds. Unlike saving (which is more about safety), investing is about risk and reward over the long run. Even beginners can start small with apps or retirement plans.

- Stocks: shares of ownership in a company. If you buy a share, you become a tiny part-owner and get to benefit if the company grows (through price increases or dividends). Stocks can go up or down in value, so there’s a balance of risk and reward.

- Bonds: Bonds are basically loans you give to companies or the government. They agree to pay you back after a set time plus interest. Bonds are generally safer than stocks, but the returns are a bit more modest.

- Index Funds: These are investment funds that copy a specific part of the stock market, like the S&P 500. Index funds spread your money across lots of companies, making them affordable and less risky for most people.

- 401k: A 401k is a retirement plan offered through your employer. You can set aside a slice of each paycheck, often pre-tax, and invest it for long-term growth. Some companies match what you put in, which is free extra money for retirement.

- IRA (Individual Retirement Account): This is a retirement account you set up outside of work. There are two main types: Traditional IRAs (contributions may be tax-deductible but you pay taxes later) and Roth IRAs (contributions are made after-tax, but you withdraw money tax-free in retirement). IRAs offer big tax perks that help savings grow faster.

- Compound Interest: This is interest that builds on both your original deposit and any interest you already earned. Over time, interest on interest helps your money grow much faster. If you start early, even tiny amounts can turn into something big thanks to compound interest.

- Diversification: Diversification means spreading your money around different investments like stocks, bonds, or funds, so you don’t lose everything if one investment does badly. It’s one of the easiest ways to help lower risk and smooth out the ride.

When you set up an investment account, pay attention to fees. Management fees, expense ratios, and transaction charges can eat away at returns, especially over long periods.

The lower your fees, the more you get to keep for yourself. Many online brokers and apps now offer commission-free trades and low-cost index funds for beginners.

If you’re investing for retirement, take full advantage of any company match—it’s like getting a pay raise just by saving for the future.

Automating your contributions is a simple hack to make sure you stay consistent without having to think about it every month.

Recommended Reading: How To Create And Track A Zero-based Budget Plan

Key Wealth Building Terms

Keeping an eye on your progress is important as you start to build wealth over time.

These six terms pop up in net worth trackers, investment guides, and money blogs.

Knowing them helps you figure out where you’re at and where you’re headed.

- Net Worth: Net worth is everything you own (cash, investments, property) minus everything you owe (debts, loans). It’s a good snapshot of your real financial health; think of it as your financial scoreboard.

- Assets: Assets are anything valuable that you own. This covers cash, your home, investments, cars; basically, if you could sell it for money or use it to pay bills, it’s an asset.

- Liabilities: Liabilities are all the things you owe, like credit card debt, car loans, student loans, or mortgages. Subtracting these from your assets gives you your net worth.

- Passive Income: Money you make without actively working for it. This can include rental income, dividends from stocks, or royalties. Growing passive income streams makes it easier to reach financial goals and get more free time.

- Active Income: Money you earn through working; think salary, hourly wages, tips, or freelance gigs. Most people start out relying on active income and then eventually add passive income sources over time.

- Financial Independence: This is when your passive income covers all your expenses, so you no longer need to rely on a job. Reaching financial independence is a milestone that allows for more freedom and choices in life.

To boost your net worth over time, look for ways to grow your assets and chip away at your liabilities. Building assets could mean investing in stocks or real estate, growing your savings, or picking up new skills that increase your earning power.

Reducing liabilities might include paying down student or credit card debt, consolidating loans for better rates, or avoiding unnecessary big-ticket purchases. The path is different for everyone, but the math is always the same: raise your assets, shrink your debts, and your net worth improves. Tracking progress monthly can motivate you, showing that even small improvements add up over time.

Financial independence isn’t just for millionaires—lots of everyday people reach it by living below their means and investing steadily. Passive income streams, like owning rental properties or building dividend portfolios, give a steady boost to your net worth without much extra effort. With patience and consistency, these habits grow stronger each year.

Start Using These Terms Today

You now have a solid handle on 30 essential personal finance terms. With this vocabulary, topics like budgeting, borrowing, saving, investing, and wealth building make a lot more sense.

Financial articles and expert advice will stop sounding like code, and decisions about your own money get less stressful because you actually know what’s being discussed.

Next, take one or two terms that match your current situation and try them out for yourself. Track your net worth (just list your assets and subtract your debts—it’s simple but super motivating). If you don’t have an emergency fund, make it a priority and stash away even $10 or $20 a week.

Don’t wait until you “know everything.”

Investing a small amount regularly or reviewing your monthly budget can make a real difference. The earlier you get comfortable, the more money habits will start working for you, even when you’re not watching.

Just knowing terms isn’t enough. It’s about putting that knowledge into practice. These words are realworld tools. Use them to take charge, ask better questions, and feel more comfortable with your money.

If you want more tips and simple explanations delivered straight to your inbox, I share new resources every week to help you keep learning.

Sign up below to get access to 4 Powerful Masterclasses Featuring 7 Figure Earners Plus a PDF Business Starter Guide for Beginners, all FREE!

Regards

Roopesh